Macro · The Fed’s Plan for the U.S. Economy

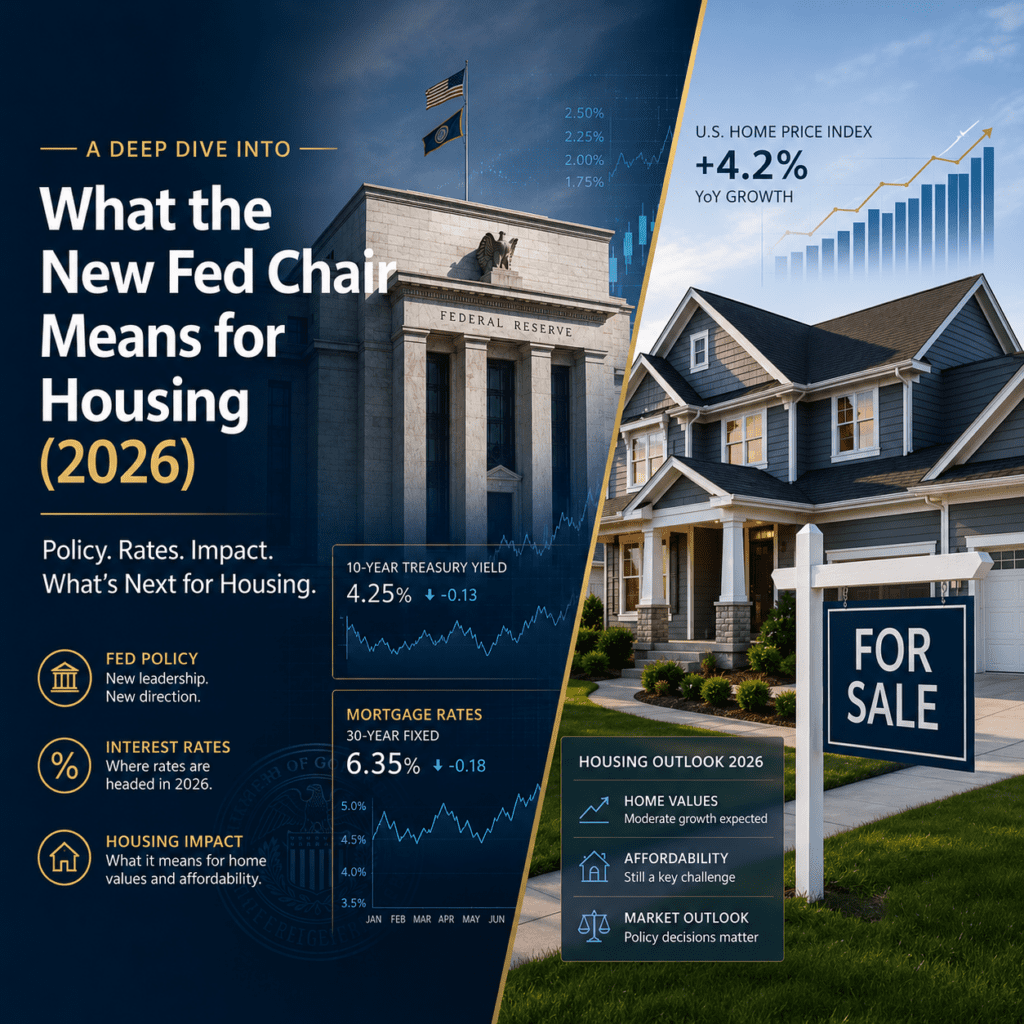

A Deep Dive Into What the New Fed Chair Means for Housing, 2026

Two events are about to collide: an Iran deal that could be signed Friday, and Kevin Warsh’s first meeting as Fed chair on Wednesday. Together they decide what happens to interest rates, the stock market, and arguably the whole economy. Here is the plan, and exactly what to watch.

By Stephen D. Ihrig II, SRA • Published June 16, 2026 • 16 min read

The short version

- Markets price a 99.6% chance of no rate change Wednesday, so the decision isn’t the news, the signal is.

- The plan: cut short rates, shrink the Fed’s balance sheet, and deregulate the banks so they absorb Treasury debt, quantitative easing by another name.

- Layer AI as a disinflation story on top, and the pitch becomes: grow out of the debt problem without inflationary pain.

- The Iran war broke it. A closed Strait of Hormuz pushes oil, inflation, and short rates up, flattening the curve the plan depends on.

- The real-asset supercycle is, per one estimate, only six years into a run that historically lasts 14 to 22.

ON THIS PAGE

- Two events, one week

- The 99.6% nobody’s watching

- The gold signal

- The plan in three steps

- The bank rule that matters

- The AI disinflation layer

- Then Iran happened

- Warsh’s two paths

- Why the deal is the plan

- The war of optics

- China adds fuel

- What to watch Wednesday

- The supercycle

- What this means for housing

- FAQ

- Key terms

- About the appraiser

The Setup

Two events, one week

The deal between Iran and the United States has, allegedly, been agreed to, with a signing supposedly set for Friday. Plenty of details could still send it south, but if it goes through, the next phase of the master plan can finally begin. Both sides say they’ve reached a framework to end the fighting; what they’re actually agreeing to, and on what timeline, is still a very big question.

Regardless of what happens Friday, the next phase of the economy starts Wednesday, June 17th, when Kevin Warsh chairs his first Federal Reserve meeting. It may be one of the most important meetings in a long time, because what he says in it will shape interest rates, the stock market, and arguably the whole economy.

FedWatch

The 99.6% nobody’s watching

Start with the CME FedWatch tool, which reads interest-rate probabilities from the market. Right now it shows roughly a 99.6% chance of no change to the federal funds rate. In other words, nothing happens to interest rates, and the market has already fully priced that in. This is not news.

MARKET-IMPLIED ODDS · WEDNESDAY’S RATE DECISION

The rate decision is a foregone conclusion. The meeting matters because of what Warsh signals, not what he does.

So why does the meeting matter? Because what Kevin Warsh says on Wednesday will matter more than what he does. To understand why, look at gold.

The Signal

The gold signal

Gold just closed below its 200-day moving average three days in a row, the longest such streak since October 2023. The last time that happened, the bond market nearly broke, the Treasury Secretary panicked and injected liquidity by buying bonds, and the price of gold went on to triple over the following two years.

I’m not saying gold is about to triple. I’m saying the last time this happened, what followed was a significant multi-year rally across gold stocks and risk assets.

Something big appears to be moving. Wednesday is when we find out which direction.

The Master Plan · via Luke Gromen, FFTT

The plan in three steps

Warsh was nominated by Trump with a clear mandate: lower interest rates so the economy grows. Jerome Powell resisted, because the U.S. has a huge debt problem. The plan is to solve that problem without triggering a crisis, and the mechanics come from a framework laid out by Luke Gromen at FFTT.

01

Lower short-term rates

The Fed only controls the short end, rates on instruments like the two-year Treasury. Cutting there makes borrowing cheaper, loosens the economy, and hands Trump a growth story heading into the midterms.

02

Shrink the balance sheet

At the same time, the Fed stops holding as many bonds. Selling bonds normally pushes long-term rates up, which sounds bad, but here it’s intentional: it creates a steeper yield curve, so banks borrow cheaply short and lend profitably long. That spread is how banks make money.

03

Deregulate the banks

The crucial step: remove the capital rules that cap how many Treasuries banks can hold, the supplemental leverage ratio. Once those limits come off, banks pile into Treasuries with leverage and absorb the bonds the Fed is selling.

The net effect on the bond market is almost identical to the Fed simply buying the bonds itself. It’s basically quantitative easing, money printing, just funneled through the commercial banking system instead of the Fed’s balance sheet.

Why route it this way? Cover. If anyone says, “The Fed is printing money again, isn’t that inflationary?” the Fed can point to its shrinking balance sheet and say no. And by lifting lending constraints, banks can do both: buy Treasuries and lend more to Main Street, so Warsh can frame it on TV as productive deregulation that helps small business, not Wall Street. There’s an element of truth to that, but the underlying machine is still money printing.

The Rule

The bank rule that matters

The regulation in step three is the supplemental leverage ratio (SLR), a post-2008 rule requiring banks to hold a capital buffer against their total assets, including Treasury bonds. Picture a bank with 100 slots for investments. The SLR says only so many can go to Treasuries, even though Treasuries are the safest asset in the world, essentially cash. They still take up slots, so banks hit a wall: they want more Treasuries, but the rule says full.

100 INVESTMENT SLOTS · BEFORE AND AFTER LOOSENING THE SLR

With the SLR cap, only 16 of 100 slots can hold Treasuries. After loosening the exemption, banks can fill 64 or more slots with government bonds, absorbing the Fed’s sales without printing money on the Fed’s own balance sheet.

Decision Tree

Warsh’s two paths

The plan works

Oil falls, inflation cools, short rates can drop without re-igniting prices. The yield curve steepens as intended. Banks absorb Treasuries. Mortgages drift back toward 6% or below.

Result: Risk-on. Stocks, gold, Bitcoin, and Gulf Coast housing all benefit.

The plan breaks

Oil stays elevated, inflation persists, Warsh can’t cut without credibility loss. The curve stays flat. Banks can’t profit on the spread. The $8 trillion Treasury refinancing gets far harder.

Result: Higher-for-longer. Mortgages stay in the mid-6% range or climb. Buyer’s markets deepen.

Local Market

What this means for housing

The key insight: mortgage rates follow the 10-year Treasury, not the Fed’s short-rate decision. The plan deliberately pushes long rates up to steepen the yield curve, so a Fed cut doesn’t automatically lower your mortgage. The Iran-driven inflation scare already lifted the 30-year fixed into the mid-6% range.

Sarasota

Buyer’s Marketmedian SFR · ~5.8-mo supply

Prices off peak, inventory elevated. Insurance costs compound rate pressure. Sellers are negotiating.

Lakewood Ranch

Balancedmedian list (core to ~$750K)

Closings jumped ~26% YoY early in 2026, suggesting the correction has largely run its course.

Bradenton / Manatee

Buyer-Friendlymedian SFR · ~4.7-mo supply

Prices roughly flat YoY as more buyers get priced out by rates and insurance, keeping inventory elevated.

Mortgage rates follow the long end of the curve. A Fed cut isn’t a mortgage cut, and on the Gulf Coast that distinction is the whole ballgame.

The housing translationQuestions

Frequently asked

What is the Fed’s “supercycle” plan?

Why does Wednesday’s meeting matter if rates won’t change?

Why is the Iran deal so important to the economy?

What is the real-asset supercycle?

What is the supplemental leverage ratio (SLR)?

How does this affect the housing market and home prices?

Reference

Key terms

- Yield curve

- The line plotting interest rates across maturities. A “steep” curve (low short rates, high long rates) lets banks profit on the spread; a “flat” curve squeezes them.

- The spread

- The gap between short- and long-term Treasury yields (here, 2-year vs 10-year). Wider spread, more bank profit and more Treasury buying.

- Quantitative easing (QE)

- Central-bank money creation used to buy bonds and push rates down. The plan reproduces its effect through banks rather than the Fed’s own balance sheet.

- Strategic Petroleum Reserve (SPR)

- The U.S. emergency oil stockpile, drawn down to cushion gas prices while Hormuz stays closed.

- DXY (the “Dixie”)

- The U.S. Dollar Index. A weaker dollar after the meeting hints at coming liquidity; a stronger one hints at tighter conditions.

- Supercycle

- A multi-decade rotation in which either financial assets or real assets dominate for 15 to 20 years before the pendulum swings.

About

About the appraiser

Stephen D. Ihrig II, SRA

State-Certified Residential Real Estate Appraiser · SDI Appraisal

Steve is the principal of SDI Appraisal. He holds the SRA designation from the Appraisal Institute and is a State-Certified Residential Real Estate Appraiser in Florida. Steve practices evidence-based valuation and has provided expert-witness testimony in the Circuit and County Courts of Florida’s Twelfth Judicial Circuit for Sarasota and Manatee Counties.

- —SRA Designation — The Appraisal Institute, Florida Gulf Coast Chapter

- —Member — Forensic Expert Witness Association (FEWA)

- —Member — Community of Asset Analysts (CAA)

- —Member — REALTOR® Association of Sarasota & Manatee

- —Specialties — luxury & waterfront, estate & divorce, date-of-death & step-up basis, price verification, pre-listing, FEMA 50% Rule, IRS casualty loss, litigation & expert witness

Not financial advice. This article is provided for educational and entertainment purposes only. Markets carry real risk of loss, figures and forecasts may change, and nothing here is a recommendation to buy or sell any asset. Do your own research and consider speaking with a licensed appraiser, financial advisor, or investment adviser before acting.

Get in touch

Request an appraisal or a consultation

Tell us about the property and the purpose of the assignment, and we’ll respond with scope, timing, and a fee quote.

SDI Appraisal prepares appraisals for estate & trust, date-of-death & step-up in basis, tax gift, divorce, pre-listing & price adjustment, price verification (cash), relocation, Actual Cash Value for the FEMA 50% Rule, and casualty loss (IRS Form 4684). Primary services include expert witness testimony, litigation support, appraisal consulting, and review of another appraiser’s work.

Serving Sarasota, Lakewood Ranch, Bradenton, Anna Maria Island, Longboat Key, Bird Key, Lido Key, Siesta Key, Casey Key, Nokomis, Venice, Manasota Key, Palmetto, Ellenton, Parrish, and St. Petersburg — across Sarasota and Manatee Counties, and areas of Charlotte and Pinellas Counties.